2020 started off with a bang for many businesses. Unfortunately, the COVID pandemic brought business growth to a screeching halt, especially for small businesses. Many qualified for PPP loans. While it helped sustain businesses through the pandemic, that funding only covered their basic operating expenses. It didn’t make up for lost revenue, nor did it provide the working capital necessary for businesses to adjust their operations to the “new normal”.

As business owners look ahead, they need to find a way to hit the ground running as restrictions lift and social distancing eases up. That’s going to take extra capital that many just don’t have. Traditional bank loans were difficult to obtain before the pandemic. For the immediate future, they are going to be even more elusive. So, where can a small business get the funding to thrive in the post-COVID marketplace? For those who lack capital in between invoicing and payment, factoring receivables can be a great option.

Factoring receivables is also known as invoice factoring or factoring. The first thing business owners need to understand is that factoring is not a loan. It is a way to get the money that is already owed to you quicker. Especially now, in the wake of the pandemic, your customer may be waiting until the day they are due to pay your invoices. By factoring those unpaid invoices, you can get most of that money now, allowing you to have the staff and equipment necessary to meet the “new normal” head-on.

When factoring receivables, you sell your unpaid invoices to a factoring company. In exchange for those invoices, factoring companies typically pay 80 to 85 percent of their face value. Once the invoices are sold, they are owed to and collected by the factoring company. Once the invoices have been paid, the business would receive the balance from the factoring company minus a previously agreed-upon fee.

It’s not unusual for a small business to have a black mark or two on its credit report. Fortunately, this isn’t an issue when factoring receivables. The factoring company will be looking at your customer’s credit history, not yours. For this reason, it’s important to submit only invoices issued to customers in good standing. So, what happens if a customer doesn’t pay a factored invoice. That depends on what type of factoring services you received.

Factoring receivables to increase your cashflow post-COVID can make it easier to regain traction in the marketplace. However, it’s important to understand the different types of factoring. The most common type offered by factoring companies is recourse factoring. With this option, the responsibility falls on the business owner if their customer doesn’t pay. With non-recourse factoring, the terms can vary but typically the bulk of the responsibility falls on the factoring company. Because the risk for the factoring company is higher, the fees for non-recourse factoring will be higher as well. While this option may provide less risk for the business owner, it also means they will receive a smaller portion of their sales once the invoice is paid.

Want to make sure your business is ready to compete in the post-COVID marketplace? CapFlow Funding Group can help make sure you have sufficient cash flow to make that happen. CapFlow Funding Group will work with you to find the best funding solution to provide your business with immediate working capital. We provide services to many different industries with a variety of different funding needs. Contact us today and find out how invoice factoring can help grow your small business.

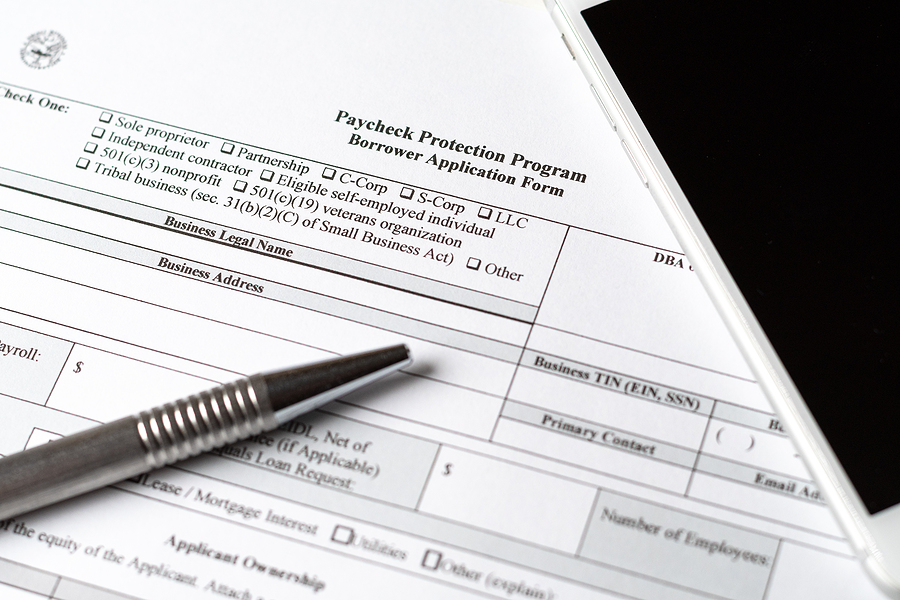

Congress finally agreed on a second stimulus package right before Christmas. The bill signed into law by the president reopened the Payroll Protection Program (PPP) with $284 billion in small business disaster relief funding. The additional funding will allow some small businesses who are still struggling to receive additional funding, referred to as a second draw loan. Like the previous round of PPP loans, these funds have the potential to be forgiven. However, the guidelines to receive loan forgiveness are different from those accompanying the first round of PPP loans and may continue to evolve as the SBA has not yet released their official guidelines. Here’s what we know so far.

Who Qualifies – The second round of PPP loans is sharpening the focus on small businesses. A company must have 300 employees or less to qualify for additional small business disaster relief. This number has been significantly reduced from the first round of PPP loans, which required the company applying for funding to have up to 500 employees. To further ensure that the disaster relief funding benefits small businesses, publicly-traded companies are barred from applying for PPP funds. Second draw PPP loans will be capped at $2 million, again significantly lower than the previous limit of $10 million. Second-time applicants will have to provide documentation that their sales fell by 25 percent in at least one quarter of 2020 as compared to the previous year. They will also need to have used or will use the full amount of their first PPP loan.

Inclusion of Non-Profit Organizations – The original PPP loans were not available to non-profits and other organizations. The small business disaster relief program has been updated to include eligibility for certain housing cooperatives, news organizations, section 501(c)(6) organizations, and Economic Injury Disaster Loan (EIDL) recipients.

How is the Loan Amount Determined? – For most applying for a second round of small business disaster relief funding, their 2019 average monthly payroll is multiplied by 2.5. This will provide applicants with enough funding to cover 2 ½ months of payroll expenses. Restaurant and foodservice businesses that are classified under the North American Industry Classification System (NAICS) beginning with the number 72 will have their loan amount calculated differently. They will have their 2019 average monthly payroll multiplied by 3.5, providing them with a larger loan amount to cover 3 ½ months. If a small business has an average monthly payroll expense of $1000, once approved you would receive $2500 in funding. A restaurant or foodservice business with the same payroll expense of $1000 would receive $3500.

Forgiveness Eligibility – Those receiving the small business disaster relief funding from the reopened payroll protection program will still be required to spend 60 percent of the funds received to cover payroll expenses. However, there are new guidelines for how the remaining 40 percent can be spent. Originally earmarked for expenses such as mortgage, rent, and utilities, the balance of the PPP loan can also be spent on the following eligible expenses.

The forgiveness process has also been simplified for loans of less than $150,000. A signed,one-page form attesting that the money was used for its intended purpose is all that’s required for PPP loans below this amount.

Taxation Updates – The first round of PPP loans were considered to be tax-free as long as they are forgiven. However, normally deductible expenses paid for with PPP funds, could not be claimed as a deduction. So, those funds were being taxed indirectly. Among the changes to the requirements and regulations governing the new round of small business disaster relief funding, forgiven PPP loans are completely tax-free. This means normally deductible expenses paid for with PPP funds can still be claimed as a deduction.

At CapFlow Funding Group, we understand that while a second draw PPP loan can be a financial lifesaver for many small businesses, navigating the rules and regulations to qualify for loan forgiveness can seem daunting. In an effort to assist our clients and other business owners, we continue to provide updates and the latest information relating to the PPP Act. Keep in mind, the Payroll Protection Program will close again on March 31, 2021.

While the pandemic has drastically altered the economic landscape, we will do our best to help our clients not only survive but successfully rebound in the” new normal”. Contact us to see how our alternative funding options may be able to help.